Jean-Claude Trichet, the president of the European Central Bank, has a love affair with fighting inflation and his shift from the debt crisis to the "I" word did wonders for the euro — at least for now. With the latest European CPI number screaming a “frightening” 2.4%, Trichet is looking into his closet and polishing his “weapons of price destruction.”

Does he have a point? Not really, but he’s savvy, and I view him as a master of public relations and manipulation. His objective is to draw attention away from the issue at hand while lending credibility and strength to the euro to attract much needed capital, not fight inflation.

Every month we eagerly await the lonely numbers, react along with the markets, and don’t have the time or patience to look back and put a few concepts in perspective. But those are the exercises that get my blood pumping, and I always end up learning something new. I start by throwing a few numbers and charts together on a white board, and then I put on my Sherlock Holmes hat and start dissecting the information and looking for fibers in the vast array of evidence. After all, it is the non-published, apparently unrelated bits of information that deliver the gold nuggets. Everything else tends to be information repackaging ... and if it's wrong, the packaging won’t correct it.

But how does the simple task of turning the knobs on money supply/interest rates controls affect the inflation rate? Or could it be that, at times, rate increases are not directed at inflation, but rather currency values that in turn assist in controlling commodity price increases, especially if they are priced in dollars? Or could it be just politics to enhance a currency in trouble and attract much needed capital? Keep in mind that Central Banks know far more of what is brewing below the surface than we do.

[Click to enlarge]

Let’s put aside the fact that CPI is unreliable, fake, manipulated, etc., and concentrate on the reality that everyone makes decisions on the numbers anyway. One can yell that inflation is much higher than stated, but that will only bring five seconds of satisfaction and cloud one’s judgment when trying to play the investment game. Okay, so the CPI is incorrect.

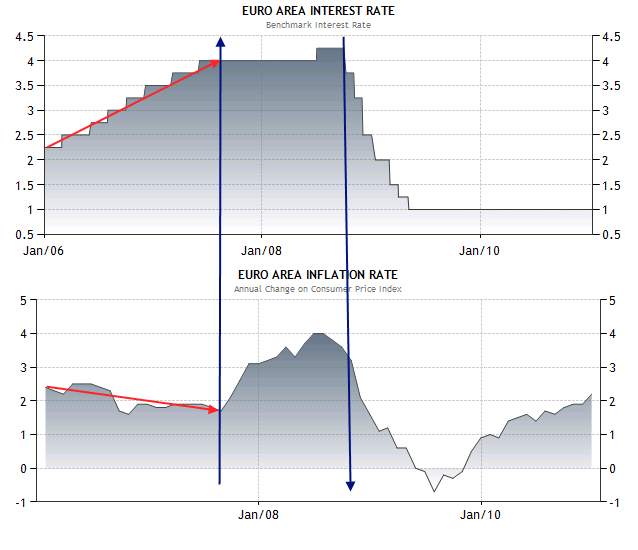

The charts above tell a story that goes to the heart of the effectiveness, if not credibility, of Central Banks. The dates are between the beginning of 2006 and the end of 2010, and depict the interest rate and inflation movements in the euro zone. The fascinating point is that inflation was contained — and declining — up until the end of 2007, the crest of the real estate wave, while rates kept rising, as if the ECB preempted the inflationary times ahead.

That’s not how it works, and we know that it takes six to nine months for rates to filter through the economy. As inflation started to rise after rates had already reached 4%, the ECB didn't become too concerned that the inflation rate was at double its target ... yet a mere 0.4% above the accepted level gets it a little hot under the collar.

Why didn't the ECB keep on increasing rates through 2008 and 2009? Because the euro was now cutting into the export machine and the law of diminishing returns was chipping away at its game. (Or it has a crystal ball.) If one wants to be cynical, the argument could be made that inflation only increased after interest rates were at a higher level; thus, high rates create inflation. That’s what the chart implies — and there are valid points in that construct.

On January 13, 2006, Bloomberg ran a story highlighting that “European Central Bank President Jean- Claude Trichet said the bank must be 'vigilant' on inflation expectations and there are 'encouraging' signs that economic growth is accelerating.” Traders were puzzled, because the markets had scaled back the probability of rate increases, but some clarification was given:

On March 2, 2006, the ECB increased the minimum bid rate from 2.25% to 2.5% since investors didn't get his message that “The Euro must rise!” Granted that according to the graph, inflation was above the target 2%, but that wasn’t the driver because inflation dropped below 2% and rate increases continued propelling the Euro to $1.60.“Trichet may have been actually temped to utilize this word again to show that there will likely be a rate increase again,'' said Julian Callow, chief European economist at Barclays Capital (BCS) in London. “I suspect today Trichet felt that he had not been so clearly understood yesterday.''

Then rates stayed constant through most of 2008 until the debt crisis became a fact. As inflation started to diminish, interest rates followed, but as inflation made a return at the end of 2009, the ECB kept rates at 1% until today. So if inflation hit 4% when rates were at 4%, inflation should be much higher now (based on an inverse relationship) and should be running at about 6-8%.

Looking back (see green rectangle in chart above), the euro was once again heading to parity with the dollar, if not below, and had been declining for one year. Then came the ECB rate increases that were prompted by anything but inflation, while the minimum bid rate had stayed at 2% since June 5, 2003; the euro also increased because the Fed lowered rates due to 9/11. Most likely, the capital flowing out of Europe into the booming U.S. real estate market triggered the defense mechanism, and Trichet knew that the euro was a bad idea and would be in trouble.

At this juncture, the ECB is once again facing the capital outflows of yesteryear, but the game is somewhat different. A lower euro actually supports a euro zone, which is far more dependent on exports than the U.S., but the environment is not conducive to higher rates. And there lies one of the biggest dilemmas for the European Union — although there are many more facets to the story. The inflation number, as rare as the instance is, is now incorrect on the wrong side of the axis, because admitting that deflation is the prevalent theme is not convenient to the ECB. Capital would flow out and undermine the currency itself. Oh yes, I’ve seen the inflation calculators all over the web, but the problem is that these “apps” are as reliable as the IQ tests that I’m constantly invited to take.

I’m not privy to Jean-Claude Trichet’s game plan, but don’t be surprised if the European Central Bank increases rates by 25 basis points on Thursday, February 3. If that happens, a monumental short-term wrench will be thrown into everyone’s investment plans. And that’s Trichet’s style!

Disclosure: I have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours.

By Carlos X. Alexandre

No comments:

Post a Comment